Ever since the 60s, real wages have remained mostly stagnant - even taking a downward trend in the past year. Although maybe our nominal wages have increased, our real wages have remained the same and even more alarming the purchasing power of income has plummeted. Even worse so, the price of food and energy has gone up in recent years and we're still working the same amount of hours, sometimes more. Where is the improvement and, most importantly, why is the middle class shrinking? Although all this issues would usually mean a rise in unionization amongst workers and rallies to demand for higher wages/benefits and perhaps more equal distribution of wealth, as happened during the Great Depression and the 1910s, union membership has actually paradoxically decreased in the last 50 years.The Bureau of Labor Statistics reports that only 6.9% of workers in the private sector are union members.

Although I've oftentimes heard the right demonize unions as dangerous to the delicate fabric of a free market, and oftentimes advocate enacting legislation to curb their power, there is no question the decrease in union membership has had a direct effect on the concentration of wealth in the United States and the middle class share of aggregate income. Here is are the results that were found by Karla Waters and David Madland of the at the Center for American Progress (CAP):

Now, before I get to the credit illusion, which is likely the culprit, first we have to dispel a few arguments against the stagnation of real wages in the United States - three of them specifically I want to talk about;

This cannot be true, hourly outputs per workers have actually been steadily increasing. This is based on information from the Bureau of Labor Statistics and Bureau of Economic Analysis; there is indeed a growing gap between output and real wages:

No, it is not. The Second Wave of feminism, which started in the early 60s, brought many more women to the workforce. It's not that the workers are bringing more real income home, it's that more people are working in the household. In an article in the journal article by Rebecca A. Clay of the American Psychological Association:

In 1940, according to the Employment Policy Foundation's Center for Work and Family Balance, 66 percent of working households consisted of single-earner married couples. By 2000, that percentage had dropped to less than 25 percent. By 2030, the center estimates, a mere 17 percent of households will conform to the traditional "Ozzie and Harriet" model.It is this phenomenon that has caused an increase in average income per household - there are now many more new sources income per family, but that doesn't necessarily tell us anything about the average real wage for each individual bringing it home.

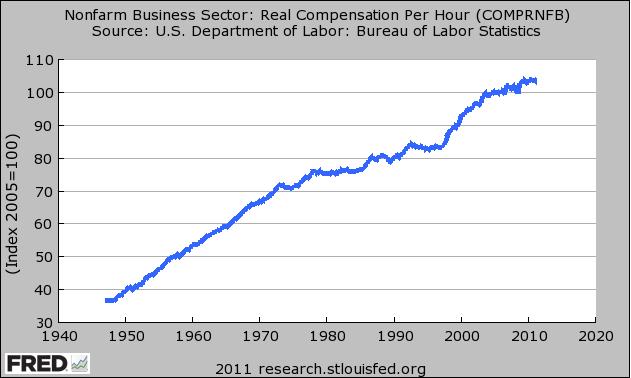

Q: You are not adding benefits to the real wage. The Bureau of Labor statistics has shown there has been a upward trend in real compensation per hour since the 1940s. Does this not explain the stagnation of wages?

However, we have to look at this data with the increase in workers' output rather than by itself. Since the year 2000, there has been especially a disconnect between real compensation per hour and output.

But this disconnect in average hourly compensation and productivity started far before the 00s; it actually began in the late 70s and got progressively worse since the Reagan years. Below is a graph from the Economic Policy Institute;

And although this graph does not show the growing gap between productivity and average hourly compensation since '07, it has gotten much worse since then. So yes, average hourly compensation has been increasing but not as nearly as the same rate as productivity has.

-------------------------------------------------------------------------------------------------------------------------------

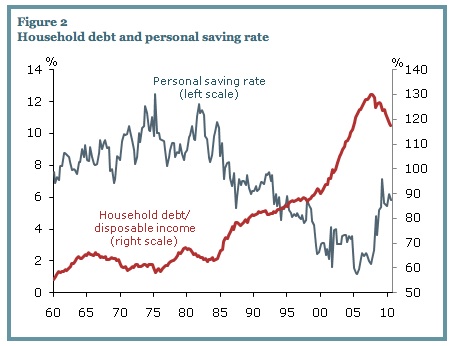

Now, for the topic of this post which may actually be shorter than the background information; Why aren't the workers mobilizing and demanding higher wages as they did in the first half of the 20th century? There are many reasons; one being the destruction of unionism during the Reagan years and another being the of spending money you don't actually have; the illusion of credit. Ever since real wages have become stagnant and the sharp decline of unionization in the 80s, there has been a sharp increase in household debt in the United States, which actually dissuades workers from demanding higher wages in some respects. It is this exploitative dichotomy that has kept corporate profits high and wages low; all in the guise of "buy now, pay later!" and 'economic growth.'

Below is a graph of household debt versus persona savings taken from 'The Basis Point,' a blog by mortgage banker Julian Hebron:

Here is a chart taken from the Federal Reserve Bank of San Francisco. It was a study pertaining to the entire United States:

Why is the middle class shrinking and being anesthetized by credit? It is this type of behavior that drives society outside of its means and gives it working class families the false perception that their wages are increases; maybe nominally they are, which is deceptive in itself, but the main hurdle we must overcome is realizing the distraction of mass consumption by credit going forward. This requires questioning this entire system which has, for the most part, become based on credit and money yet to be paid. I highly fear the collapse of this 'credit culture' and the shaky foundation it is built on; And perhaps worst of all, we are unjustly condemning future posterity to debt bondage. What happened during the crisis of 2008 we may find to become a staple in the modern 21st century economic model; and since debt wasn't properly liquidated, worse may be yet to come. The functionality of such an illusionary market method I am highly skeptical of, and its outcome will most definitely hurt the current mainstream liberal capitalist model.

No comments:

Post a Comment